What Is Bankability in BESS?

Bankability describes whether a company, a project, or a piece of equipment carries low enough risk to be financed, insured, and contracted on acceptable terms. There is no universal score or certification — the word describes an assessment, and that assessment is different depending on who is making it and what they are evaluating.

In BESS, the term is used constantly. Developers refer to the bankability of their projects. Manufacturers refer to the bankability of their companies — both technically and commercially. EPCs present their track record, financial stability, and delivery capability as markers of bankability. The concept applies to every company in the value chain — but what makes a company bankable depends on what products and services they provide, and the perspective from which they are being assessed.

Where Bankability Is Assessed

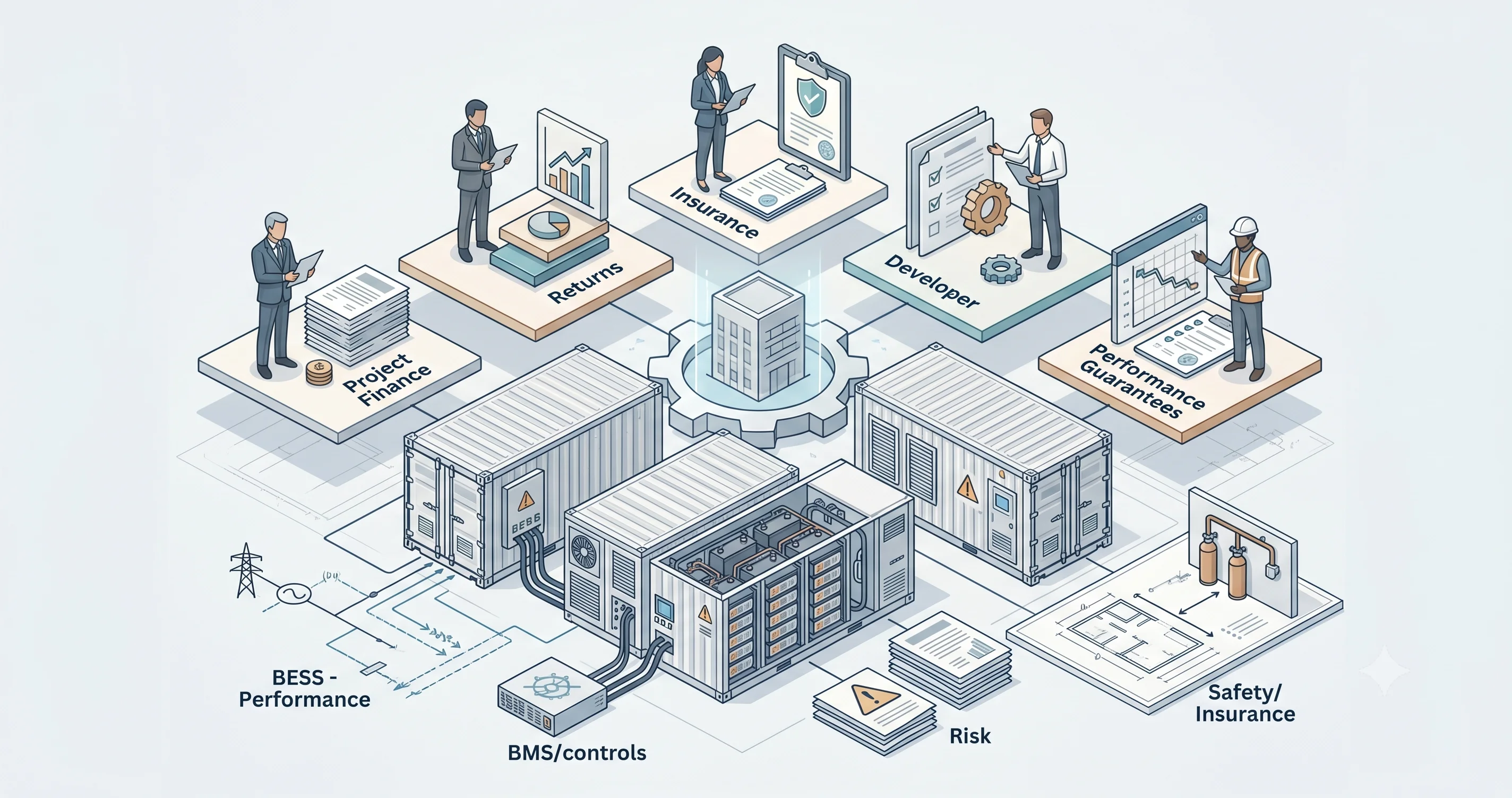

Bankability is assessed at multiple levels simultaneously, and a weakness at any level can block the entire project.

At the project level, bankability depends on the revenue structure, counterparty quality, delivery model, and insurance program holding together well enough for a lender to write a loan against the project’s expected cash flows.

At the equipment level, it depends on whether the manufacturer’s track record, financial strength, product maturity, certifications, and regional service capability together present low enough risk for the project to be financed and insured without a cost-of-capital penalty.

At the EPC level, it depends on whether the contractor’s delivery track record, balance sheet, and bonding capacity can back the guarantees in the contract.

At the insurance level, the project must be insurable. Cell chemistry, separation distances between DC blocks, fire testing certification, and supplier acceptance all affect whether a project can be insured and at what premium. Without an insurance program in place, no lender will close.

A project can have bankable equipment from a bankable manufacturer, delivered by a bankable EPC, and still fail to close if the revenue structure doesn’t work for lenders or if the site layout doesn’t work for insurers. Bankability is not one assessment — it is a stack of assessments that must all resolve at the same time.

What BNEF Tier 1 Actually Measures

BloombergNEF publishes a quarterly Tier 1 list for BESS suppliers. It has become one of the most recognized bankability signals in the industry — and one of the most frequently used in manufacturer marketing materials.

The criteria vary by year, but one consistent principle is that a manufacturer cannot count projects that have been financed — directly or indirectly — by the manufacturer itself. A company cannot finance its own reference projects and use them to demonstrate bankability. The list reflects whether independent, third-party lenders have been willing to finance projects using that manufacturer’s equipment.

What the list does well is filter out suppliers with no track record in genuinely financed projects. It reflects market consensus and updates frequently enough to capture shifts.

What it does not measure is product quality. It does not measure financial strength. It does not assess regional fit or reflect recent safety incidents. A manufacturer can be on the Tier 1 list and still be rejected by a specific lender for a specific project because of geography, chemistry, contract terms, or insurance requirements.

The most common misuse is treating the list as a pass-or-fail verdict — as if inclusion means a manufacturer is bankable and exclusion means they are not.

Bankability Is Dynamic

A project that was bankable at financial close can become difficult to refinance if performance falls short, if market conditions shift, or if the counterparty structure weakens. A manufacturer that was bankable two years ago may not be today if their financial position has deteriorated or if an incident has changed insurer appetite. An EPC contractor that was bankable in one market may not be in another where they have no track record.

Bankability is built over time — from origination through financial close and into operations — and it can be lost. Treating it as a one-time checkbox rather than an ongoing condition is one of the most common mistakes in BESS project development.