Hybrid vs. Co-Located BESS: What's the Difference?

Developers, investors, and equipment manufacturers across the battery energy storage industry use hybrid and co-located interchangeably, as if they describe the same thing. They do not. The distinction comes down to metering and settlement, and it has direct consequences for grid fees, trading strategy, financial modeling, and how the grid operator treats the plant.

What Hybrid and Co-Located Have in Common

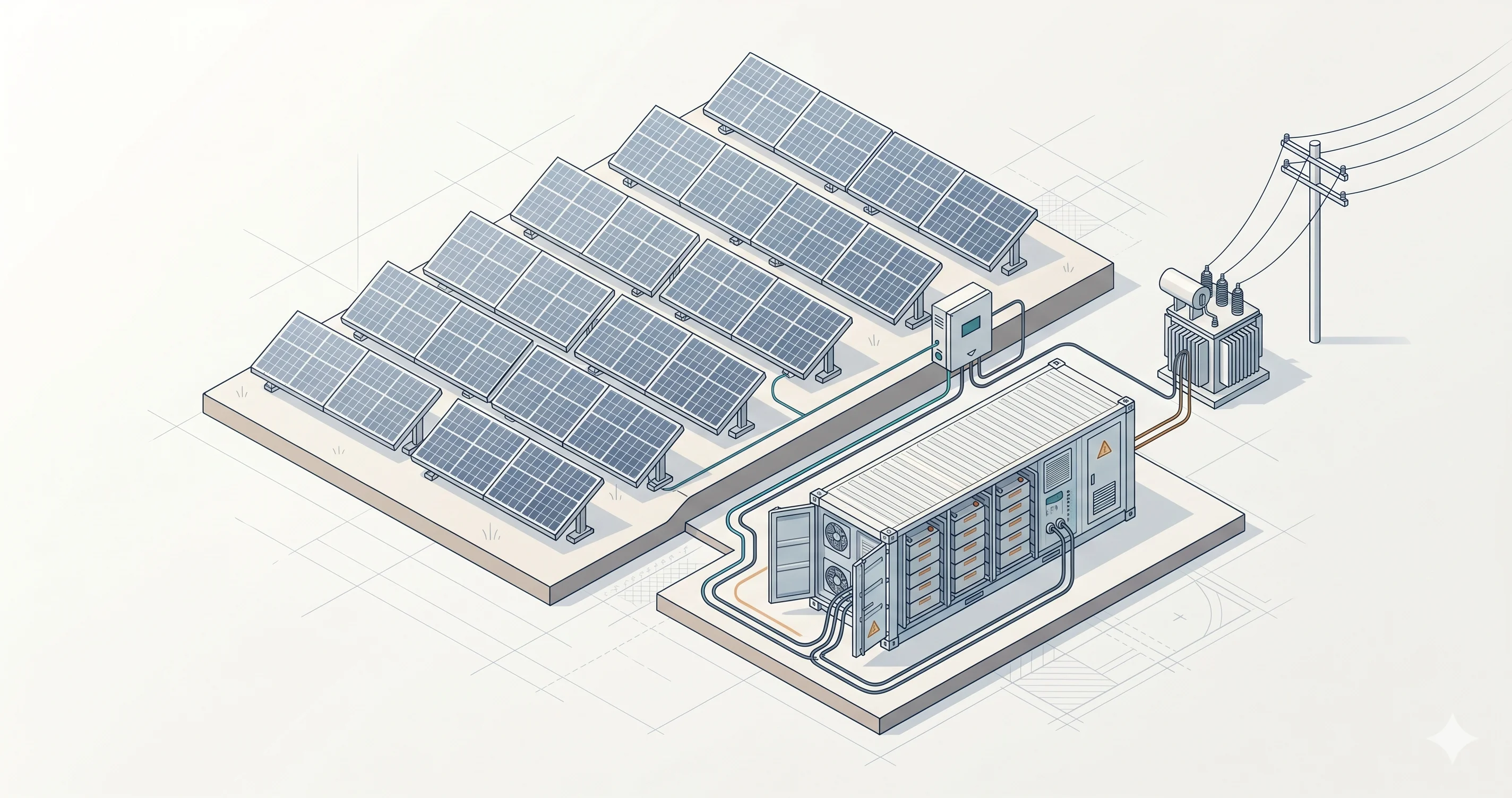

Both configurations combine a generation asset — usually a PV plant or wind farm — with a BESS plant at the same site. Both share the same Point of Interconnection (POI) with the grid.

The difference is not in the physical layout. Two plants with identical equipment, identical capacity, and identical site designs can be classified differently depending on how the metering and settlement are structured. That structure determines whether the grid operator sees one plant or two.

Hybrid: One Settlement Meter, One Plant

In a hybrid configuration, the combined facility has a single settlement meter at the Point of Interconnection. The grid operator sees one plant. It does not see the individual assets behind the meter — it only sees the net output at the POI.

The DSO may still require meters on the individual assets for grid compliance and monitoring, but these are not used for settlement. Internal energy flows between the generation asset and the BESS plant are not measured or settled by the grid operator. If the PV charges the battery, and the battery later discharges to the grid, the grid operator does not know which asset produced the energy at any given moment. Because no energy crosses a settlement boundary, internal transfers do not trigger grid fees or taxes.

A hybrid power plant requires a Hybrid Power Plant Controller (HPPC) that sits above the individual asset controllers. The HPPC receives dispatch instructions and distributes PQ setpoints to the PV power plant controller and the BESS power plant controller. It manages the combined output to stay within the limits of the grid connection agreement.

Co-Located: Separate Settlement Meters, Separate Assets

In a co-located configuration, each asset has its own settlement meter and its own market registration with the grid operator. The PV plant and the BESS plant are metered independently. The grid operator sees two assets sharing a point of interconnection.

If the PV charges the BESS plant, that energy passes through both settlement meters. It is exported from the PV plant’s meter and imported through the BESS plant’s meter. Depending on the market rules — defined by the DSO or TSO — this internal energy transfer may trigger grid fees or taxes that would not apply in a hybrid configuration.

There is no HPPC in a co-located setup. Each asset operates under its own dedicated power plant controller. Each asset is contracted, dispatched, and settled independently.

The Distinction in One Sentence

A hybrid power plant has one settlement meter and is treated as a single facility by the grid operator. A co-located plant has separate settlement meters per asset and each asset is treated independently.

Everything else — grid fees, trading constraints, financial modeling assumptions, controller architecture — follows from this.

A Concrete Example: 80 MW Point of Interconnection

To make the distinction tangible, consider a site with an 80 MW discharge capacity at the Point of Interconnection.

Hybrid Configuration

The site has 80 MW of PV and a 10 MW / 40 MWh BESS plant, all behind one settlement meter. The facility is registered as a single hybrid unit. The grid connection agreement caps discharge at 80 MW at the POI.

The installed capacity is effectively 90 MW. But the grid operator only allows 80 MW of export at any given moment. This creates a direct trading constraint: if the PV is generating at full power, the BESS plant cannot discharge at all. The POI cap is already reached.

The HPPC manages dispatch across both assets, but it is limited by the POI. During peak solar hours, when PV output is close to 80 MW, the HPPC might instruct the BESS plant to charge from excess PV instead — storing energy to discharge later when PV output drops and the POI has headroom.

The grid connection agreement may also include a consumption allowance — for example, 10 MW — so that the BESS plant can charge from the grid. This allows the BESS plant to participate in balancing services even when PV output is low and grid charging is needed.

If a route to market (RTM) provider — an optimizer or trader — has committed the BESS plant to a balancing service product, the HPPC must reserve enough capacity to meet that obligation while still managing the PV output. The BESS plant does not trade freely. It trades around the PV.

Co-Located Configuration

The same 80 MW POI, but now allocated differently: 70 MW for the PV plant and 10 MW for the BESS plant. Each asset has its own settlement meter, its own market registration, and its own contract with the grid operator.

The BESS plant has its own 10 MW allocation and can trade without restriction within that allocation. There is no HPPC coordinating dispatch between assets. Each asset operates independently under its own power plant controller.

That simplicity comes at a cost.

The PV plant is limited to 70 MW, even though the POI allows 80 MW. During peak solar hours, the PV may discharge at its full 70 MW. But outside those hours — early morning, late afternoon, cloudy periods — a significant portion of that 70 MW allocation goes unused. The grid connection is not fully utilized.

This underutilization is a key drawback of the co-located structure. The POI capacity is pre-allocated per asset, and whatever one asset does not use, the other cannot reclaim. In the hybrid configuration, the full 80 MW is shared dynamically. In the co-located configuration, 70 MW belongs to the PV whether the PV needs it or not.

Why It Matters in Practice

Getting hybrid and co-located wrong — or treating them as the same thing — creates problems that surface in financial models, grid connection applications, and commercial negotiations.

Financial Modeling

A hybrid revenue model must account for the HPPC’s dispatch logic and the interaction between assets — the BESS plant’s tradeable windows depend on PV output. A co-located revenue model works with fixed capacity allocations per asset, but must account for POI underutilization outside peak generation hours. Modeling a co-located plant as if it were hybrid, or vice versa, will produce incorrect revenue projections.

Grid Fees and Taxes

The same energy flow — PV charging the BESS plant — is treated differently depending on the configuration. In a hybrid structure, that energy never crosses a settlement boundary. In a co-located structure, it passes through two settlement meters and may be treated as a grid transaction, triggering fees, taxes, or levies. A BESS plant that charges primarily from the co-located PV may still incur grid fees on that energy, while the same flow in a hybrid structure would incur none.

Existing PPAs and Retrofit Scenarios

When a BESS plant is added to an existing PV site with a long-term PPA, the choice between hybrid and co-located is often constrained by the existing contract.

The PV plant already has its own settlement meter tied to the PPA. Restructuring this into a hybrid arrangement means the settlement meter now measures the combined output of both assets. This may require renegotiating the PPA terms and introducing operational constraints that the original contract was not designed to accommodate. The off-taker’s settlement changes. The metering changes. The contractual framework may need to change with it.

Co-location avoids this problem. The PV keeps its own settlement meter, its own PPA, and its own market registration. The BESS plant is added alongside it with separate metering and separate contracts. Both assets trade as individual units.

For sites with existing contracted generation, co-location is often the more feasible path — not because it is technically superior, but because it avoids disrupting existing commercial arrangements.

Grid Connection Availability

When a BESS plant is added to an existing renewable site, the grid operator may not approve an increase in discharge capacity. The grid connection was designed and permitted for the original generation asset, and additional export capacity may not be available.

Often, the only path forward is a consumption allowance: the BESS plant can charge from the grid, but the site cannot exceed its original discharge power at the POI. Whether this constraint results in a hybrid or co-located structure depends entirely on the DSO or TSO and their rules for metering, registration, and treatment of internal energy flows.

Jurisdiction Defines the Structure

The same physical plant design, with the same equipment and the same site layout, can be classified as a hybrid power plant in one jurisdiction and a co-located plant in another. The classification is not determined by the hardware. It is determined by the DSO or TSO rules for metering, asset registration, market participation, and the treatment of internal energy flows for grid fees and taxes.

Some markets only allow a hybrid registration for combined assets behind a single POI. Others offer both structures — hybrid and co-located — with different regulatory treatments for each. The choice, where it exists, has direct consequences for how the plant can be operated, traded, and settled.

This means that general statements about “hybrid BESS” or “co-located BESS” are incomplete without specifying which market and which regulatory framework applies. A configuration that avoids grid fees in one country may trigger them in another. A trading strategy that works under hybrid registration may not be possible under co-located registration, even for an identical plant.

Who Needs to Understand This

The distinction between hybrid and co-located affects decisions across the project lifecycle. RTM providers need it to model revenue accurately. Developers need it to structure grid connection agreements. EPCs need it to design the right control architecture. Asset owners and investors need it to evaluate returns on comparable terms.

An investor comparing two projects — one hybrid, one co-located — cannot use the same assumptions. The POI utilization profile, the grid fee exposure, and the revenue model mechanics are fundamentally different.